Executive Summary

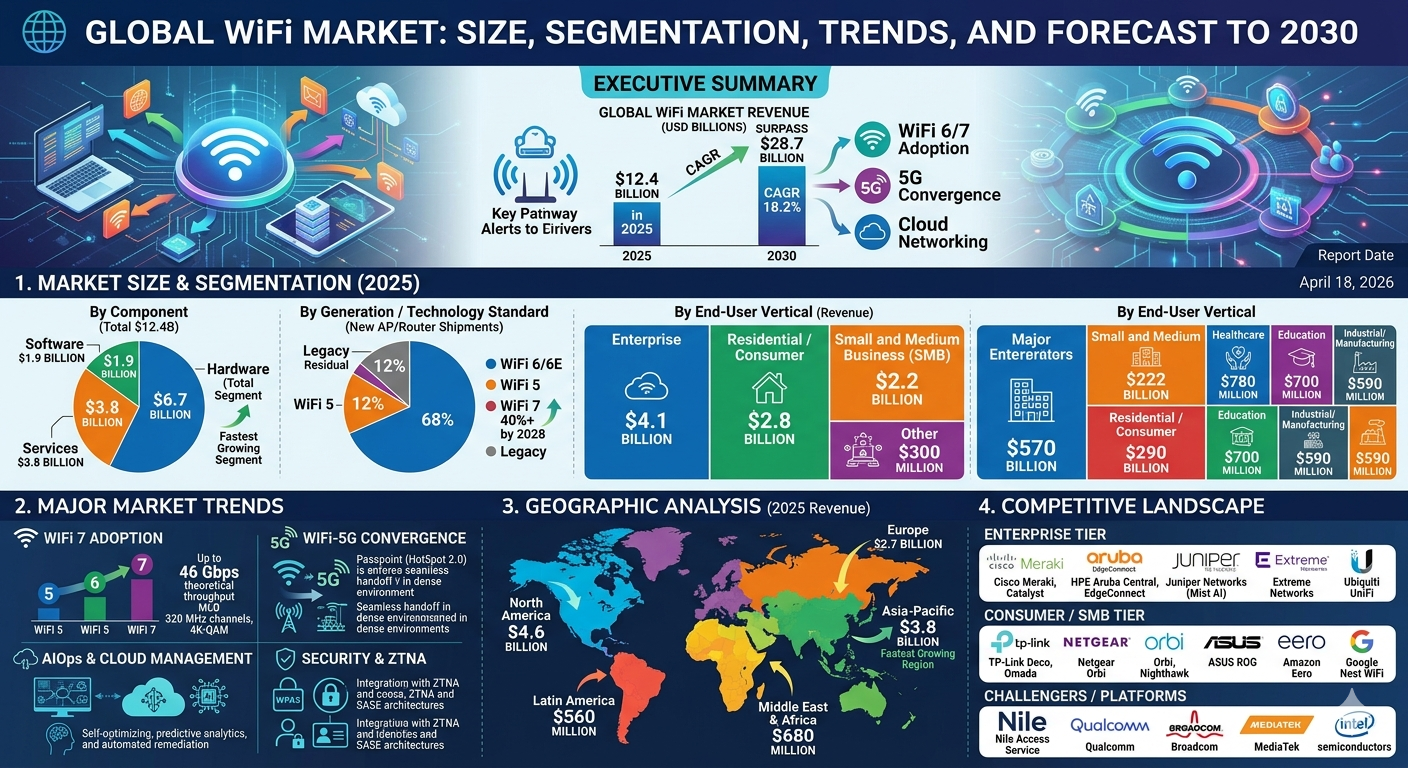

The global WiFi market stands at an inflection point. Valued at approximately $12.4 billion in 2025, the market is on a trajectory to surpass $28.7 billion by 2030, registering a compound annual growth rate (CAGR) of roughly 18.2% over the forecast period. This growth is not merely a function of incremental device proliferation; it is driven by a fundamental restructuring of how connectivity is architected, monetized, and consumed across enterprise, residential, industrial, and public environments.

WiFi 6 (802.11ax) has crossed from early adoption into mainstream deployment, while WiFi 7 (802.11be) is moving from specification to commercial rollout with a speed and density capability that will render prior generations obsolete in high-demand environments. Simultaneously, the convergence of WiFi with cellular (particularly 5G), the maturation of cloud-managed networking, and the explosive growth of IoT endpoints are reshaping competitive dynamics across every tier of the ecosystem — from silicon vendors and OEM hardware manufacturers to managed service providers and software platform operators.

This report provides a comprehensive assessment of the global WiFi market: its current size, primary segmentation vectors, demand drivers, restraints, competitive landscape, and a five-year forecast through 2030. It is intended as a reference document for strategic planners, investors, operators, and technology decision-makers operating in or adjacent to the wireless connectivity space.

1. Market Definition and Scope

For the purposes of this report, the WiFi market encompasses the full value chain of IEEE 802.11-standard wireless LAN technology. This includes:

- Hardware: Access points (APs), wireless routers, wireless LAN controllers, mesh networking nodes, and WiFi-integrated chipsets and modules.

- Software: Network management platforms, cloud controllers, security software, analytics and assurance tools, and AI-driven optimization engines.

- Services: Managed WiFi services, installation and integration, professional services, support contracts, and WiFi-as-a-Service (WaaS) subscriptions.

The scope spans consumer (residential), enterprise (SMB and large enterprise), industrial/manufacturing, government/public sector, hospitality, healthcare, retail, education, and outdoor/public access deployments. Geographic coverage is global, with dedicated breakouts for North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

Revenue figures represent end-market spending (sell-through to end customers), not component-level shipments unless otherwise noted. All figures are expressed in USD at constant 2025 exchange rates.

2. Market Size and Historical Context

2.1 Current Market Valuation

As of 2025, total global WiFi market revenue is estimated at $12.4 billion, with hardware representing the largest share at approximately 54% of total market value ($6.7 billion), followed by services at 31% ($3.8 billion) and software at 15% ($1.9 billion). The software segment, while smallest in absolute terms, is growing fastest — a reflection of the broader industry shift from capex-heavy hardware procurement toward subscription-based, cloud-managed architectures.

Between 2019 and 2025, the market grew from an estimated $6.8 billion, implying a historical CAGR of approximately 10.5%. This growth was significantly shaped by three exogenous forces: the COVID-19 pandemic (which dramatically accelerated residential and enterprise WiFi upgrades between 2020 and 2022 as remote work and hybrid schooling became permanent fixtures), the regulatory push for spectrum availability in the 6 GHz band (enabling WiFi 6E), and the ongoing enterprise digital transformation cycle that positioned reliable wireless connectivity as core infrastructure rather than a supplementary utility.

2.2 Unit Shipments and ASP Dynamics

Annual WiFi-enabled device shipments — including routers, access points, and mesh systems — exceeded 1.1 billion units in 2025, with consumer devices accounting for roughly 72% of volume. However, enterprise access points command significantly higher average selling prices (ASPs): enterprise APs average between $300 and $800 per unit depending on tier and standard generation, versus $80 to $200 for consumer-grade mesh nodes and residential routers. This ASP differential is why enterprise accounts for a disproportionate share of revenue relative to unit volume.

WiFi 6 and 6E chipsets now represent the majority of new AP shipments, displacing WiFi 5 (802.11ac) as the baseline specification in both consumer and commercial channels. WiFi 7 shipments, while still a small percentage of the total, are growing rapidly and are expected to constitute approximately 35% of enterprise AP shipments by 2027.

3. Market Segmentation

3.1 Segmentation by Generation / Technology Standard

WiFi 5 (802.11ac): Now in a managed decline phase. WiFi 5 still dominates the installed base, particularly in residential and SMB environments where refresh cycles are slow. However, new WiFi 5 product introductions have nearly ceased, and the standard is increasingly relegated to low-cost, price-sensitive applications. Market share in new shipments fell below 20% in 2025 and is forecast to drop below 10% by 2027.

WiFi 6 / 6E (802.11ax): The current mainstream. WiFi 6 delivers up to 9.6 Gbps theoretical throughput (vs. 3.5 Gbps for WiFi 5), with key advances in multi-user MIMO, OFDMA, and target wake time for IoT power efficiency. WiFi 6E extends operation into the 6 GHz band, unlocking 1,200 MHz of additional clean spectrum and enabling the low-latency, high-density performance demanded by enterprise video conferencing, AR/VR workloads, and dense IoT deployments. In 2025, WiFi 6/6E accounts for approximately 68% of new AP and router shipments globally.

WiFi 7 (802.11be): The emerging high-performance tier. WiFi 7 achieves theoretical throughputs exceeding 46 Gbps via 320 MHz channels, 4K-QAM modulation, and multi-link operation (MLO), which allows simultaneous transmission across multiple bands and channels to reduce latency and improve reliability. Commercial deployments began in earnest in late 2024, primarily in flagship smartphones, high-end routers, and enterprise APs from Cisco, Juniper (Mist), HPE Aruba, and Ubiquiti. WiFi 7 represented approximately 12% of new shipments in 2025 and is on track to reach 40%+ by 2028.

WiFi 4 and legacy (802.11n and earlier): Residual installed base only. No meaningful revenue contribution in new deployments. Ongoing only as replacement demand in very low-cost or developing-market applications.

3.2 Segmentation by End-User Vertical

Enterprise (Large and Mid-Market): The highest-value segment, accounting for approximately $4.1 billion or 33% of total 2025 market revenue. Enterprise buyers demand managed, scalable, and secure wireless infrastructure with centralized visibility, policy enforcement, and integration with broader network security stacks (ZTNA, SASE, SD-WAN). Cloud-managed WiFi from vendors such as Cisco Meraki, Juniper Mist, HPE Aruba Central, and Extreme Networks dominates new enterprise deployments. AIOps capabilities — using machine learning to predict failures, automate remediation, and optimize channel assignments — have become a critical differentiator in enterprise procurement.

Small and Medium Business (SMB): A large and underserved segment in transition. SMBs have historically been served by prosumer-grade equipment or basic ISP-provided hardware, but cloud-managed platforms are now penetrating this tier aggressively, driven by simplicity, lower TCO, and integrated security features. The SMB segment represents approximately $2.2 billion in 2025 and is growing faster than the large enterprise tier as managed service providers (MSPs) increasingly offer WiFi-as-a-Service bundles.

Residential / Consumer: The largest segment by unit volume but lower in revenue density. Consumer WiFi spending is estimated at approximately $2.8 billion in 2025 for hardware (routers, mesh systems, range extenders), with additional revenue flowing through ISP-managed premises equipment and retail retail channels. Mesh networking systems — dominated by Eero (Amazon), Google Nest, TP-Link Deco, Netgear Orbi, and Linksys Velop — have substantially displaced traditional single-router architectures in mid-to-high-income households. The consumer segment is more sensitive to macroeconomic conditions and ISP subsidization policies than the enterprise segments.

Healthcare: A specialized and high-growth vertical, valued at approximately $780 million in 2025. Healthcare WiFi demands address unique requirements: clinical-grade reliability (no dropped connections for biomedical device telemetry or real-time imaging data), HIPAA-compliant segmentation, support for location services (RTLS for asset tracking and patient flow), and integration with healthcare IoT — from infusion pumps and ventilators to nurse call systems and mobile carts. The shift toward connected care, telehealth infrastructure, and smart hospital initiatives is accelerating WiFi refresh cycles in this vertical.

Education: Driven by 1:1 device programs, hybrid learning models, and large-scale campus deployments, education represents approximately $700 million in 2025. K-12 and higher education institutions are in active refresh cycles, with many upgrading to WiFi 6E to handle the density of student devices in lecture halls and dormitories. Government subsidy programs (such as the FCC E-Rate program in the United States) continue to fund infrastructure upgrades, though funding timelines introduce lumpiness into annual spending patterns.

Hospitality: Hotels, resorts, and convention centers represent a resilient and premium-density market for WiFi infrastructure. Guest experience expectations — shaped by residential mesh and high-speed home broadband — have dramatically raised the performance bar for hotel WiFi. Revenue from this vertical is estimated at approximately $620 million in 2025, with strong growth tied to post-pandemic travel recovery, premium tier expansion, and the growing role of WiFi in enabling smart room automation and guest mobile engagement platforms.

Retail: Brick-and-mortar retail WiFi serves dual purposes: customer-facing guest access and operational connectivity for POS systems, inventory management, digital signage, and loss prevention. Omnichannel retail transformation — blurring physical and digital commerce through RFID, autonomous checkout, and mobile-POS — is driving WiFi upgrades across major retailers. This vertical accounts for approximately $540 million in 2025.

Industrial / Manufacturing / Logistics: One of the fastest-growing verticals, expanding at above-market CAGRs as Industry 4.0 digitization programs mature. Industrial WiFi must operate in harsh RF environments (metal-dense factories, high-interference warehouses), support time-sensitive networking (TSN) for automation equipment, and interoperate with private 5G in converged wireless environments. Revenue is estimated at approximately $590 million in 2025, with significant growth projected as brownfield industrial facilities complete digital overhauls.

Government and Public Sector: Encompasses federal agencies, municipal networks, public transit, and smart city deployments. This segment is characterized by long procurement cycles, strict security certification requirements (FedRAMP, FIPS 140-2), and increasing interest in outdoor WiFi infrastructure for smart city and public safety applications. Revenue is estimated at approximately $420 million in 2025.

3.3 Segmentation by Deployment Architecture

Cloud-Managed WiFi: The dominant and growing architecture for enterprise and commercial deployments. Cloud-managed platforms centralize configuration, monitoring, policy management, and analytics in cloud-hosted controllers, eliminating on-premises controller hardware and enabling zero-touch provisioning. This model has shifted WiFi purchasing from a capital expenditure to a software subscription model, with annualized recurring revenue (ARR) profiles benefiting vendors and introducing greater revenue predictability. In 2025, cloud-managed architectures account for approximately 58% of enterprise WiFi revenue, up from roughly 35% in 2020.

Controller-Based (On-Premises): Traditional enterprise architecture, declining in share but still relevant for high-security environments (air-gapped networks, government classified deployments) and large organizations with existing controller investments. This segment is expected to continue its decline, constrained to specialized use cases and very large installed-base refresh cycles.

Controllerless / Standalone: Dominant in consumer, SMB, and small branch deployments. Mesh networking systems fall primarily into this category, as do most residential routers. While this architecture lacks centralized management, modern intelligent mesh systems increasingly incorporate cloud-optional management capabilities, blurring the line with cloud-managed tiers.

WiFi-as-a-Service (WaaS): An emerging but rapidly growing model in which operators and MSPs deliver fully managed WiFi infrastructure — hardware, software, monitoring, and support — as a monthly or annual subscription. WaaS is particularly attractive to mid-market enterprises and hospitality operators who prefer operational expenditure models and lack in-house networking expertise. The WaaS segment is projected to grow at a CAGR exceeding 25% through 2030.

3.4 Segmentation by Component

Access Points (APs): The core hardware unit of the market. Enterprise APs (indoor and outdoor) represent the majority of commercial WiFi hardware revenue. The market is bifurcating between high-density, multi-radio APs for flagship deployments and lower-cost single or dual-radio APs for cost-sensitive environments. WiFi 6E and WiFi 7 tri-band APs command significant ASP premiums.

Wireless LAN Controllers: Physical controllers are in structural decline, replaced by cloud controllers and virtual network functions (VNFs). Residual demand is concentrated in on-premises enterprise environments and government deployments.

Routers and Gateways: Relevant primarily in consumer and SMB channels. The integration of router and gateway functions into ISP-provided CPE is moderating retail router revenue, though premium mesh system upgrades remain a healthy consumer spending category.

WiFi Chipsets and Modules: The semiconductor layer is dominated by Qualcomm (Wi-Fi 7 Networking Pro platform), MediaTek (Filogic series), Broadcom (BCM series), and Intel (integrated laptop/PC WiFi). Chipset revenue, while not always captured in end-market WiFi figures, is a critical upstream indicator of generational technology transition timing.

Software and Platforms: Network management software, security overlay platforms, analytics engines, and location services software collectively represent the fastest-growing component category. The shift to SaaS-licensed network management is driving software revenue growth at CAGRs of 20–25%, well above the market average.

Services: Professional services (design, deployment, integration), managed services, and support contracts represent a stable, high-margin revenue stream. Managed WiFi services are growing fastest within this component as enterprises outsource network operations to focus on core business functions.

4. Geographic Analysis

4.1 North America

North America is the largest regional market, accounting for approximately $4.6 billion (37%) of global WiFi revenue in 2025. The United States drives the overwhelming majority of this, with Canada a modest secondary contributor. The region benefits from high broadband penetration, large enterprise IT spending, and a mature ecosystem of vendors, system integrators, and MSPs. The FCC’s opening of the 6 GHz band for unlicensed use in 2020 gave the United States a head start on WiFi 6E adoption that is now reflected in the installed base. Enterprise cloud-managed WiFi penetration is highest in North America, as is adoption of AIOps-driven network management.

Key growth drivers specific to the region include federal infrastructure funding (through programs like the BEAD initiative for broadband expansion), continued enterprise digital transformation, and the maturation of WaaS delivery models through MSPs. Competitive pressure is intense, with all major vendors — Cisco, Juniper, HPE, Ubiquiti, Netgear, and emerging challengers — competing aggressively for enterprise refresh cycles.

4.2 Asia-Pacific

Asia-Pacific represents approximately $3.8 billion (31%) of global revenue in 2025 and is the fastest-growing region, forecast to surpass North America in absolute market size by 2029. China is the dominant market, accounting for approximately 45% of regional revenue, but also the most insular — domestic vendors (Huawei, H3C, Ruijie) dominate the Chinese market, and Western vendors have minimal presence. Japan, South Korea, Australia, and India are the next-largest markets, each with distinct demand profiles.

India represents one of the highest-potential growth opportunities globally, driven by rapid digitization of SMBs and public sector, government smart city initiatives, and the expansion of 4G/5G infrastructure that is creating demand for WiFi offload capacity in dense urban environments. Southeast Asian markets (Indonesia, Vietnam, Thailand, Philippines) are also expanding rapidly, driven by hospitality, retail, and enterprise growth.

4.3 Europe

Europe accounts for approximately $2.7 billion (22%) of global revenue. The market is mature in Western Europe (Germany, UK, France, Netherlands, Nordics) and transitional in Central and Eastern Europe. European WiFi adoption is shaped by stringent data protection regulations (GDPR), which affect how guest WiFi data is captured and managed, and by a relatively fragmented enterprise market served by both global vendors and strong regional integrators.

The EU’s spectrum harmonization for the 6 GHz band — completed in 2022 — enabled WiFi 6E rollout, though at a lower power ceiling than the United States, moderately constraining outdoor range performance. Public WiFi investment has been supported by EU Digital Compass initiatives, and smart building and Industry 4.0 programs are generating meaningful industrial WiFi demand across the continent’s manufacturing heartland.

4.4 Latin America

Latin America represents approximately $560 million (4.5%) of global revenue in 2025. Brazil is by far the dominant market, followed by Mexico, Colombia, and Chile. The region is price-sensitive, with SMB and residential markets dominated by value-tier hardware from TP-Link, Intelbras (Brazil), and regional distributors. Enterprise WiFi spend is concentrated in financial services, retail, and hospitality verticals. Growth is steady but constrained by macroeconomic volatility, currency risk, and lower enterprise IT maturity compared to North America and Europe.

4.5 Middle East and Africa

The Middle East and Africa (MEA) region accounts for approximately $680 million (5.5%) of global revenue in 2025. The GCC countries (Saudi Arabia, UAE, Qatar) are the highest-value sub-market, driven by ambitious smart city programs (NEOM, Dubai Smart City), premium hospitality infrastructure, and strong government spending on digital transformation. Government Vision programs across Saudi Arabia and the UAE are creating significant infrastructure investment cycles that benefit enterprise WiFi vendors. Sub-Saharan Africa remains underpenetrated, with growth largely tied to telecom operator deployments and institutional (education, healthcare) WiFi expansion funded by development programs.

5. Key Market Trends

5.1 The Transition to WiFi 7 and the Multi-Gigabit Era

WiFi 7 represents the most significant generational leap in wireless LAN performance since the transition from WiFi 4 to WiFi 5. Its defining innovation — multi-link operation (MLO) — allows devices to simultaneously transmit and receive across multiple bands (2.4 GHz, 5 GHz, and 6 GHz), dramatically reducing latency and improving reliability in congested RF environments. Peak throughput of 46 Gbps, while a theoretical ceiling, translates into practical multi-gigabit real-world performance that supports 8K video streaming, high-fidelity AR/VR headsets, and dense simultaneous device connections without performance degradation.

For enterprises, WiFi 7 enables the elimination of wired connections for many workloads previously requiring ethernet, reducing cabling costs and enabling more flexible workspace reconfiguration. The first wave of WiFi 7 enterprise AP products — from Cisco (Catalyst 9100 series), Juniper Mist (AP47), HPE Aruba (AP 730 series), and others — began shipping in 2024 and 2025, with enterprise refresh cycles expected to accelerate through 2027 and 2028.

5.2 WiFi and 5G Convergence

The historic boundary between WiFi and cellular is eroding. 3GPP standards have formalized mechanisms for WiFi/5G interworking, and enterprise private 5G deployments increasingly coexist with WiFi in industrial and campus environments — each serving complementary roles based on mobility requirements, coverage geometry, and device type. Some use cases favor cellular (wide-area outdoor coverage, high-mobility forklifts and AGVs, mission-critical latency); others favor WiFi (dense indoor coverage, cost-sensitive IoT, high-throughput stationary devices).

Passpoint (HotSpot 2.0), EAP-SIM-based authentication, and neutral host network models are enabling seamless handoff between WiFi and cellular in operator-managed environments, particularly in large venues (stadiums, airports, convention centers) where cellular capacity is insufficient to handle peak crowd loads. The convergence trend is also driving investment in unified management platforms that can orchestrate both WiFi and private cellular from a single pane of glass.

5.3 AI-Driven Network Operations (AIOps for Wireless)

AIOps has moved from marketing terminology to a genuine product differentiator in enterprise WiFi. Machine learning models trained on network telemetry data can now predict AP failures before they occur, automatically optimize channel assignments and transmit power in real time, identify anomalous client behavior indicative of security threats, and dramatically reduce mean time to resolution (MTTR) for connectivity issues — often resolving problems before end users perceive them.

Juniper Mist’s AI-driven WiFi platform is widely regarded as the most mature implementation of this capability, and the model has forced Cisco, HPE Aruba, Extreme Networks, and others to accelerate their own AI-driven assurance investments. The competitive differentiation is shifting from hardware performance specifications to the sophistication of software and data intelligence stacks, reinforcing the trend toward subscription-based platform monetization over one-time hardware margin.

5.4 Security as a First-Order WiFi Requirement

The proliferation of ransomware, supply chain attacks, and nation-state intrusions targeting enterprise networks has elevated wireless security from a compliance checkbox to a board-level priority. WPA3 adoption is accelerating, but enterprise security architectures are increasingly moving beyond protocol-level encryption toward zero trust network access (ZTNA) models in which every WiFi-connected device is continuously authenticated and authorized regardless of its network position.

Cloud-managed WiFi platforms are uniquely positioned to enforce ZTNA policies at the wireless edge, integrating with identity providers (Okta, Microsoft Entra ID) and security service edge (SSE) platforms to apply granular, per-user, per-device access controls. The integration of WiFi management with broader SASE (Secure Access Service Edge) architectures is becoming a primary enterprise purchasing criterion, directly benefiting vendors with comprehensive platform portfolios over point-solution hardware vendors.

5.5 Mesh Networking Maturation in Consumer and SMB Markets

Whole-home mesh networking has completed its transition from premium novelty to mainstream expectation in mid-to-high-income consumer markets. The replacement of single-router architectures with two- or three-node mesh systems has meaningfully increased consumer WiFi ASPs and attachment rates. Platform-level differentiation — through parental controls, cybersecurity subscriptions, network insights, and smart home integration — is giving vendors like Eero, Google Nest, and TP-Link additional recurring revenue streams beyond hardware.

In the SMB market, the same mesh and cloud-management capabilities are being packaged by MSPs as managed connectivity services — a market segment growing at above-average CAGRs as small business owners increasingly prefer all-inclusive monthly fees to the complexity of managing networking equipment themselves.

5.6 Location Services and WiFi Sensing

Fine Timing Measurement (FTM) protocols embedded in WiFi 6 and 7 enable sub-meter indoor positioning accuracy — a capability with substantial commercial value across retail analytics, healthcare asset tracking, industrial inventory management, and smart building occupancy optimization. WiFi-based real-time location services (RTLS) are displacing Bluetooth BLE beacon systems in many high-value applications due to infrastructure reuse (existing AP deployments) and accuracy improvements.

Emerging WiFi sensing capabilities — using RF signal perturbation analysis to detect motion, presence, and even physiological signals (breathing, fall detection) without cameras — represent a nascent but potentially disruptive application layer that could expand the addressable market for WiFi infrastructure well beyond conventional connectivity use cases.

5.7 Sustainability and Energy Efficiency Mandates

Enterprise and governmental procurement increasingly requires vendors to demonstrate energy efficiency, device longevity, and responsible supply chain practices. WiFi 6’s Target Wake Time (TWT) feature, which allows IoT devices to schedule transmission windows and remain in deep sleep otherwise, can extend battery life by orders of magnitude — a critical consideration for large-scale IoT deployments. Network operators are also rationalizing AP density to minimize energy consumption, enabled by the improved coverage efficiency of WiFi 6E and 7.

6. Competitive Landscape

6.1 Enterprise Tier

Cisco Systems remains the dominant enterprise WiFi vendor globally, with its Meraki cloud-managed platform and Catalyst enterprise AP lines commanding the largest installed base in large enterprise and mid-market segments. Cisco’s integration of WiFi with its broader SD-WAN, ZTNA, and ThousandEyes network intelligence portfolio creates meaningful switching costs and cross-sell opportunities. However, Cisco faces pressure from faster-moving competitors with superior AI-driven operations capabilities and more aggressive pricing.

Juniper Networks (Mist) is widely regarded as the technology leader in enterprise WiFi, with the Mist AI platform setting the benchmark for AIOps-driven wireless management. Following Juniper’s acquisition by HPE (completed in 2024), the combined HPE Juniper entity represents a formidable challenger to Cisco’s enterprise dominance, combining Aruba’s strong SMB and distribution channels with Mist’s AI differentiation. Integration execution risk remains a key variable in the combined entity’s competitive trajectory.

HPE Aruba Networks was already the number-two enterprise WiFi vendor before the Juniper acquisition. Aruba Central’s cloud management platform and the EdgeConnect SD-WAN portfolio give it strong positioning in converged enterprise networking. The HPE/Juniper combination makes this the most significant competitive development in the enterprise WiFi market in a decade.

Extreme Networks has carved out a strong position in education, healthcare, and sports venue deployments, with its ExtremeCloud platform and Universal AP architecture offering hardware flexibility across cloud, on-premises, and co-managed deployment models.

Ubiquiti continues to occupy a distinctive market position — delivering enterprise-grade performance and cloud management at price points well below the traditional enterprise tier. Ubiquiti’s UniFi platform has substantial penetration in SMB, education, and technically sophisticated prosumer deployments, and the vendor’s lack of a traditional sales force and channel structure enables its aggressive pricing. In the mid-market, Ubiquiti has consistently gained share from Cisco and HPE.

6.2 Consumer and SMB Tier

The consumer tier is dominated by TP-Link (including its Deco mesh and Omada SMB lines), Netgear, ASUS, and Amazon’s Eero. Google Nest WiFi remains significant in the consumer segment. Chinese vendors (TP-Link, Xiaomi, Huawei for non-US markets) dominate on volume and price, while premium positioning is occupied by ASUS’s ROG gaming-focused systems and Netgear’s Orbi Ultra-performance line.

TP-Link’s US market position has been subject to scrutiny over national security concerns, with congressional and executive branch actions creating regulatory uncertainty that could materially affect its North American market access. This represents both a risk to TP-Link’s business and an opportunity for competitors in the SMB and consumer segments.

6.3 Emerging Challengers and Ecosystem Dynamics

The software-centric shift in WiFi is enabling new entrants — particularly in cloud management, AIOps, and security overlay categories — to compete without manufacturing hardware. Vendors like Nile Access Service (a WiFi-as-a-Service pure-play), Celona (private wireless convergence), and various security-first networking startups are competing at the platform layer, often integrating with or displacing incumbent hardware vendors’ management stacks.

Hyperscaler involvement is also notable. Amazon’s Eero acquisition and integration with Ring, Alexa, and AWS ecosystem creates a consumer-to-cloud data flywheel that traditional networking vendors struggle to replicate. Google’s WiFi ambitions — expressed through Nest WiFi and potential integration with Google Workspace and Android enterprise management — similarly leverage platform adjacencies beyond the capability of pure networking vendors.

7. Market Drivers and Restraints

7.1 Primary Growth Drivers

Accelerating IoT proliferation: The number of WiFi-connected IoT devices is growing faster than any other device category. Smart building sensors, industrial automation endpoints, connected healthcare devices, retail point-of-sale systems, and consumer smart home devices are all adding to the demand for WiFi infrastructure density and capacity. Gartner estimates that enterprise IoT device counts will exceed 20 billion globally by 2027, with a large portion requiring WiFi connectivity.

Hybrid work permanence: The normalization of hybrid work has fundamentally altered both residential and enterprise WiFi demand. Enterprises are deploying higher-density WiFi in office environments to support fluctuating occupancy patterns and heavier video conferencing loads, while simultaneously investing in home office connectivity solutions for distributed workforces. This dual demand dynamic sustains spending across both consumer and commercial segments simultaneously.

Enterprise digital transformation: The elimination of wired infrastructure in agile workspace environments, the deployment of wireless point-of-care systems in healthcare, the rollout of self-checkout and mobile POS in retail, and the automation of manufacturing floors all depend on reliable, high-capacity WiFi. As digital transformation programs mature from pilot to full production deployment, associated WiFi infrastructure investments grow correspondingly.

New spectrum availability: The 6 GHz band opened by regulators in the United States, UK, EU, and a growing number of additional jurisdictions provides clean, interference-free spectrum that dramatically improves WiFi performance in congested environments. Additional spectrum discussions — including potential expansion in the upper 6 GHz and lower 7 GHz ranges — could further extend the capacity advantage of WiFi over constrained cellular spectrum.

7.2 Market Restraints

Macroeconomic sensitivity of enterprise IT budgets: Enterprise WiFi refresh cycles are discretionary expenditures that are postponed during periods of budget constraint. The rate environment of 2023–2024 created meaningful headwinds for enterprise networking capex, and while conditions have eased, CFO-level scrutiny of large infrastructure refreshes remains elevated.

Geopolitical risk in the supply chain: WiFi hardware is overwhelmingly manufactured in Asia (primarily China and Taiwan), creating supply chain vulnerability to geopolitical disruption. The Sino-American technology decoupling is creating bifurcated product ecosystems, complicating procurement for global enterprises and creating regulatory uncertainty for vendors dependent on Chinese manufacturing or distribution.

Spectrum regulatory fragmentation: While 6 GHz opening has been a major enabler in key markets, the regulatory landscape remains fragmented globally. Countries that have not yet harmonized their 6 GHz allocations constrain WiFi 6E and 7 performance in those geographies, creating a patchwork of product configurations and limiting the uniformity of the global market transition.

Commoditization pressure in hardware: The maturation of each WiFi generation accelerates hardware commoditization, compressing margins for vendors unable to differentiate through software and services. The entry of aggressive Asian hardware manufacturers at low price points — and the competitive threat to TP-Link potentially creating market share redistribution rather than value creation — is a structural challenge to market revenue growth relative to unit growth.

8. Five-Year Market Forecast (2025–2030)

The global WiFi market is projected to grow from $12.4 billion in 2025 to $28.7 billion in 2030, a CAGR of approximately 18.2%. This forecast assumes continued enterprise digital transformation investment, successful WiFi 7 adoption cycles, and the maturation of WaaS and cloud-managed subscription models. Downside scenarios — tied to a global recession, major supply chain disruption, or regulatory action against key market participants — could reduce the 2030 figure to approximately $21 billion. Upside scenarios — driven by faster-than-expected WiFi 7 adoption, significant new spectrum availability, or accelerated IoT deployment — could push the addressable market toward $33 billion.

Software and services will outpace hardware throughout the forecast period, rising from a combined 46% of revenue in 2025 to approximately 58% by 2030. Within software, AIOps platforms, security overlay tools, and location services will be the highest-growth subcategories. Within services, WaaS and managed WiFi will grow at above-market CAGRs, driven by mid-market and SMB adoption.

Geographically, Asia-Pacific will overtake North America as the largest regional market by approximately 2029, driven primarily by India’s infrastructure build-out and continued enterprise digitization across Southeast Asian economies. North America will retain the highest revenue density (spending per enterprise and per household), while MEA will register the fastest regional CAGR on a smaller absolute base.

By technology generation, WiFi 7 will account for approximately 55% of new AP shipments by 2030, with WiFi 6/6E representing most of the remainder. WiFi 5 will be effectively retired from new deployments, persisting only in legacy-constrained and very low-cost market segments.

9. Strategic Implications

For technology vendors, the WiFi market’s software pivot demands platform investment and recurring revenue model transformation. Vendors that remain hardware-centric will face inexorable margin compression; those that successfully build differentiated software platforms — particularly around AIOps, security integration, and location services — will capture disproportionate value in the decade ahead.

For enterprises, the WiFi infrastructure decision is no longer primarily a networking decision — it is a data and security architecture decision. The choice of WiFi platform determines the quality of network telemetry available for security monitoring, the sophistication of available automation and self-remediation capabilities, and the flexibility to integrate with broader SASE and zero-trust frameworks. Vendor evaluation criteria should weight these capabilities at least as heavily as hardware performance specifications.

For investors, the WiFi market’s structural growth profile — driven by technology generational cycles, IoT endpoint proliferation, and the enterprise digital transformation imperative — supports a durable long-term growth thesis. The most attractive investment vectors are software and SaaS-oriented players (cloud management, AIOps, security-adjacent), WaaS pure-plays targeting the underserved SMB tier, and semiconductor vendors positioned to lead the WiFi 7 and beyond chipset transition.

For regulators and policymakers, the WiFi market’s dependence on unlicensed spectrum allocation makes continued and expanded spectrum access a critical policy lever. The United States’ early and broad 6 GHz opening has provided measurable economic and performance advantages; extension of similar policies globally would accelerate adoption of high-performance WiFi in markets currently constrained by spectrum limitations.

10. Conclusion

The WiFi market is not a commodity connectivity market in structural maturity — it is a high-growth technology platform undergoing fundamental transformation across every dimension: generational technology cycle, deployment architecture, business model, and competitive structure. The convergence of WiFi 7 performance capabilities, AI-driven network intelligence, zero-trust security integration, and subscription-based delivery models is creating a market that rewards differentiation and penalizes commoditized hardware positioning.

The $28.7 billion market projected for 2030 will be structurally different from the $12.4 billion market of today — more software-rich, more services-oriented, more tightly integrated with security and AI infrastructure, and more globally distributed. The vendors, operators, and investors who recognize this transformation and position accordingly will be the primary beneficiaries of what remains one of the most durable and pervasive infrastructure growth stories in the global technology sector.

Methodology Note: Market size estimates are derived from analysis of public financial disclosures from major market participants, industry association data (Wi-Fi Alliance, IEEE), regulatory filings, channel data from major distributors, and primary research conducted with enterprise IT buyers, MSPs, and system integrators across North America, Europe, and Asia-Pacific. All estimates reflect MarketAnalysis.com’s independent analytical judgment and should not be attributed to any single third-party data source. Forecasts reflect base-case assumptions and are subject to revision as market conditions evolve.

Related:

- From Inventor to Follower: How the West Ceded WiFi’s Cutting Edge to China

- 60 GHz WiGig Is Not Dead: Here Is Where It Actually Makes Sense

- 802.11r, 802.11k, 802.11v: The Three Protocols That Make WiFi Roaming Seamless

- HaLow (802.11ah): The Sub-1 GHz WiFi Standard Built for IoT That Nobody Talks About

- How Enterprise WiFi Authentication Actually Works: 802.1X and RADIUS Explained

- How to Read Your WiFi Signal Strength: What dBm Numbers Actually Mean

- Mesh WiFi vs Access Points: Which Architecture Is Right for Your Home

- Multi-Link Operation Explained: How WiFi 7 Uses Multiple Bands Simultaneously

- Reconfigurable Intelligent Surfaces: The Coming Upgrade to Indoor WiFi Coverage

- The Comprehensive WiFi Guide

- The Hidden Math Behind WiFi Speed Claims: What 9.6 Gbps Really Means

- The KRACK Attack: What It Was, What It Taught Us, and Where WPA2 Stands Today

- The Right Way to Plan WiFi Channels in a Dense Apartment Building

- What Is OFDMA and Why It Makes WiFi 6 Better in Crowded Spaces

- What Is WiFi 8? Multi-AP Coordination and Why It Changes Everything

- Why Open WiFi Networks Are No Longer Necessarily Dangerous (OWE and Enhanced Open)

- Why Your 5 GHz WiFi Is Faster But Shorter-Range Than 2.4 GHz

- Why Your Smart Home Devices Should Be on a Separate WiFi Network

- Why Your WiFi Router Should Never Be on the Floor

- WiFi 6 vs WiFi 6E vs WiFi 7: What Actually Changed and What It Means for You

- WiFi Calling Quality Problems? The Real Culprit Is Usually Not Signal Strength

- WPA3 vs WPA2: What Changed and Whether You Need to Upgrade